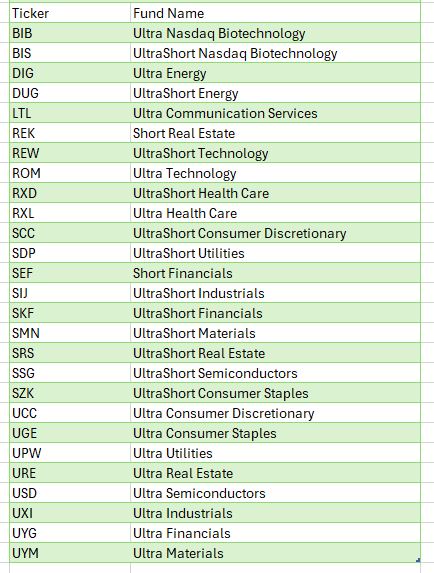

There are many ETF families in the market today, and of course, the oldest and most popular ETF, SPY has been around since 1993. Ultra ProShares Exchange Traded Funds (ETFs) developed by Profunds and traded on the AMEX. are one of the most actively traded areas of the markets. With $billions pouring into the UltraShort QQQ ETF, QID, it’s evident that it’s become one of the most actively traded ETFs globally.

Whether you’re a trader or investor, these Ultra ETFs serve as valuable tools capable of enhancing returns while mitigating risks.

Ultra bullish and UltraShort ETFs on broad market indices expanded some years ago to include leveraged bullish and bearish Sector and International ETFs. These additions enable investors to hedge or amplify sector exposure effortlessly. Moreover, these Ultra and UltraShort ETFs are compatible with IRAs or retirement accounts, where shorting or margin trading is typically restricted.

From a trader’s perspective, the liquidity and leverage of Ultra Bullish and UltraShort ETFs, which move two times the underlying index or inversely track it, offer a simpler and less risky alternative to options, futures, or shorting stocks.

For day traders, the highly liquid QQQ ETFs, QLD and QID, along with S&P500 ETFs, SDS and SSO, have become favored vehicles. The volatility of these ETFs presents opportunities for swift gains.

For investors and portfolio managers, ProShares ETFs offer a plethora of risk management tactics and asset allocation strategies. They provide flexibility to hedge against market risk or capitalize on market fluctuations. Furthermore, leveraging Ultra ETFs in asset allocation frees up capital for further diversification, allowing for strategic positioning across various sectors and markets. Sectors, in particular, have gained importance in recent times, with ProShares Sector ETFs offering exposure to Dow Jones Sectors.

For further leveraging the leverage, listed options on Ultra ETFs bring new possibilities for creative strategies. Covered call writes on bearish ETFs or options on Ultra ETFs provide avenues for managing risk and capitalizing on market movements with added leverage.

Given these ‘options on steroids’ move so quickly, only spend as much as you can afford to lose keeping in mind the thought “Have a hunch – buy a bunch. Hunch is wrong – bunch is gone”. While using Puts or Calls on Ultra Short and Ultra ETF’s requires some upside down and out-of-the-box thinking they add are few arrows to the trader’s quiver.

In conclusion, the Ultra ProShares ETFs have revolutionized trading and investing, offering opportunities previously inaccessible to individual investors.

I hope all of you are keeping healthy in this pandemic. Some of you may have had the COVID-19 virus or have a family member who may have contracted it, but for the most part as a whole, we are working together to get through this and doing okay.

RECAP:

Last month I illustrated the previous time we have a virus that was similar to the Coronavirus, and that was the Spanish Flu back in 1918. It was a horrible time where more than 51 million and some estimates are up to 100 million people died. More than 675,000 people died from the Spanish flu in the U.S. It infected more than 50 million people worldwide and was a disaster. There was very little anyone could do during that time, and there was little medicinal relief. The Spanish Flu is called the most significant medical holocaust in history. And yet the stock markets in this country fell 34% from the beginning of the flu to the lowest part in the stock market. A year later, it went up 80% approximately from its low to its high. Am I saying this will happen again? No, I’m not planning on it, but if the world recovered from a 50 million person loss and a massive pandemic it had when the world population was much smaller, then we should recover and move beyond this as well.

Over the last month, the stock and bond markets, especially the NASDAQ, have soared with the NASDAQ now up 1.66% for the year. The reason is that with most people confined to their homes, stocks like Amazon, Google, Netflix, Facebook, Microsoft, Zoom, DocuSign, and more are being used, contributing to their earnings and revenues dramatically. Stocks like Airlines, cruise ships, restaurants, manufacturing, and many more are not doing well. That is why you will see below that the sectors in terms of which areas are declining and which are growing are very different.

CURRENT TRENDS:

The growth sector has done relatively well, but only a few large companies have contributed. These few large companies are why the Equal Weighted S&P 500 is -16.2% but the regular S&P is down 9%. I continue to like the large tech and health care companies, the NASDAQ is nearing the end of its game, and it is not much below its high it hit in February. The Midcaps are down 18-23% this year, and particular issues have more of a potential move upward, in my opinion. A year or two out from this point, I think this sector and the markets should be nicely higher. Can it go down from here into the fall and winter if we have a second wave down? Absolutely, but it is an excellent time to add money to your equity side in a diversified portfolio over the next 6 months. Many people are doubling up their contributions on a monthly basis. If you are more than five years before retirement, you may want to think about doing something similar. If stocks are cheap then isn’t it smart to buy when they are reasonably priced if over the long term the market should be higher?

Have we gone down this much over the last 50 years? Yes, many times. Has it recovered each time? Yes. Because capitalism works and good companies over the long term make money, we are all in this together.

Some of the INDEXES of the markets both equities and interest rates are below. The source is Morningstar.com up until May 8, 2020. These are passive indexes. Dow Jones -14.0% S&P 500 -9.0% EQUAL WEIGHTED S&P 500 -16.1% NASDAQ Aggressive growth +1.66% I Shares Russell 2000 ETF (IWM) Small cap -20% Midcap stock funds -18-23% International Index (MSCI – EAFE ex USA -19.0% Financial stocks -27% Energy stocks -34% Healthcare Stocks -.50%

Moderate Mutual Fund Investment Grade Bonds (AAA) Long duration -8.5% High Yield Merrill Lynch High Yield Index -9.4% Floating Rate Bond Funds -7.3% Short Term Bond -3.52% Fixed Bond Yields (10 year) .68% Yield As you see above, the only index doing well is Large tech. You should have this sector, but most everything else is starting to recover.

Classicalprinicples.com and Robert Genetskis Excerpts:

After soaring a week ago, stock prices turned mixed. The Nasdaq and Nasdaq 100 were up 1% and 4%, while the S&P 500 and Dow fell 1%, and small caps were down 2% to 4%.

The economic collapse in April has led forecasters to revise downward estimates of the decline in output, employment, and profits. Last week I expected the economy would begin to recover in May. It will. Unfortunately, ongoing restrictions from Governors and the stimulus bill will limit the initial stage of the recovery. Due to these current restrictions, means the economy will not show signs of a meaningful recovery until June at the earliest.

As a result, the financial damage to the economy in terms of lost output, jobs, wages and salaries, profits and debt will continue for another month

While several technology companies are holding up well, non-tech companies are suffering. And few companies are willing to guide earnings.

The 800-pound gorilla continues to be the outlook for the virus. Containing the spread of the virus remains a crucial problem.

Some countries and states succeed without a lockdown, while others are less successful. Due to the differing results, it raises the near-term uncertainties over how quickly the economy can recover. If setbacks occur, stocks will be vulnerable.

Despite a 15%+ unemployment rate in April and probably higher in May, the stock prices continue to anticipate better times and a recovery in the markets. I am optimistic longer term for the stock markets, although the short term could be more volatile.

Dr. Genetski’s opinion is that every person and circumstance is different. There are no guarantees expressed or implied in any part of this correspondence. Source: Classical Principles.com

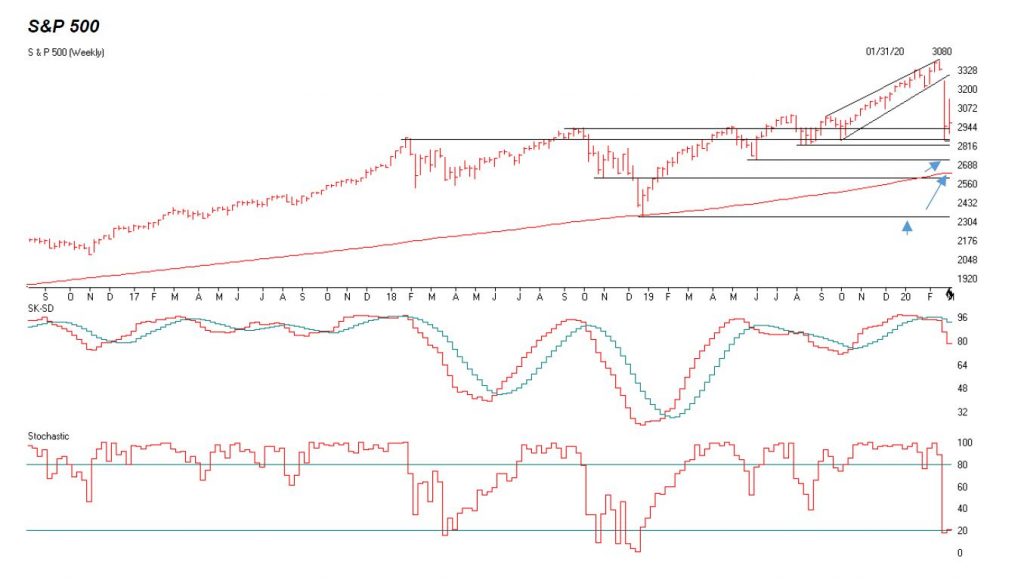

DOW JONES

As you can see the Dow went down to the 18,300 level and has risen to the 50% Fibonacci Level at 23,901. In other words when markets decline, they tend to retrace much of the decline at the 23.8%, the 50% the 61.8% and the 78.6% level and stall and reverse. Notice at the 23901 level the Dow tended to hang around there for a couple of weeks and tried to go up to the next level at the 25236 level. This is the next level where the Dow Jones could stall if it keeps rising. The Dow Jones is made up of a lot of large industrial, and value stocks that have really not participating in the rally as much as the NASDAQ tech stocks seen on the next page. Watch for a trend line break of 23901 to confirm another down leg to the 22565 if it is on big volume. This is short term. Long term I am still positive over the next 2 years or so, when we get a vaccine and a treatment, and more herd immunity.

The SK-SD stochastics model. If it is above the 88 level like it is now the market is a little over bought and this means don’t buy now short term. Volume over the last month or so the market has been rising on low volume. This means people are afraid to commit and there may not be a lot of conviction on the rally.

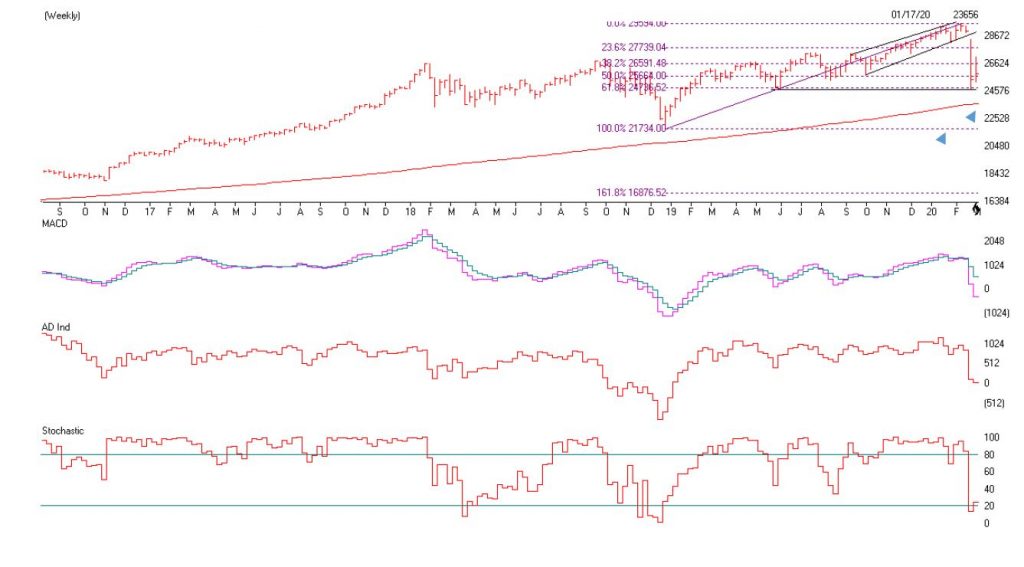

NASDAQ QQQ

The true Champ this year again has been the NASDAQ. These stocks include, Facebook, Amazon, Docusign, Paypal, Mcrosoft, Netflix, etc. All of the stocks that benefit by you and your businesses being home. This QQQ are the top 100 NASDAQ stocks and is now up 3% plus for the year while everything else in the normal world is down 16-38%. The QQQ is now getting a little OVERBOUGHT so I would not go out and buy a bunch of tech stocks here. In fact, the QQQ is approaching a pretty substantial resistance level. The first is a gap fill and could bring the QQQ to 230.55 and reverse or it could reach its old high of 237 and reverse. Longer term I think it will break through the old high, but we are now getting to a point I think the QQQ has gone up as far as it should. So watch the 230.55 to fill the gap and reverses or the old high of 237 area.

The SK-SD Stochastics is overbought just like it was in the Dow Jones. The Momentum indicator gave a Buy signal at the blue arrow as it as the pink crossed the blue line, if it crosses the blue lien going down it is a SELL. This large tech area is still long term bullish, but short term I would take a few chips off the table as an index. The midcap, small cap and large cap value sector has a lot more to recover.

If the QQQ falls or closes below 216.8 or breaks the trend line I am getting Cautious to very Cautious.

SUPPORT LEVELS:

Support levels on the S&P 500 area are 2882, 2796, 2649, and 2500. These might be accumulation levels, especially 2649, or 2500. 2936 and 3015 is resistance. Support levels on the NASDAQ are 9036, 8612, and 7856 Topping areas 9323 to 9573. On the Dow Jones support is at 23,901, 22,569, and 20912. Topping areas 25,236 and 27,077. These may be safer areas to get into the equity markets on support levels slowly on the accumulation areas.

THE BOTTOM LINE:

The market has rebounded nicely over the last month mainly on the NASDAQ tech stocks that benefit from people staying at home and using all of the tech companies to their benefits. This stay “at home” policy has increased demand for technology, and why the internet stocks have done so well. The other part of the markets from the financial to energy and other value stocks are still down from 18-33%. It is all about the growth sector that is benefiting the most. Over the long term, I am very bullish on the market, but over a short time, I can see a topping or sideways to down on the large growth companies as they are now reasonably priced. If the market continues to do well, I would expect the Midcaps to start to outperform. But there is a caveat. There are trend-line right below the markets, and if they are broken and close below those areas, then the markets could start a correction again. Trend-lines are essential to hold. If they don’t hold, then there could be a setback to support the levels stated above. I still like the USA market better than the international one.

Best to all of you,

Joe Bartosiewicz, CFP® Investment Advisor Representative 5 Colby Way Avon, CT 06001 860-940-7020 or 860-404-0408

SECURITIES AND ADVISORY SERVICES OFFERED THROUGH SAGE POINT FINANCIAL INC., MEMBER FINRA/SIPC, AND SEC-REGISTERED INVESTMENT ADVISOR.

Charts provided by AIQ Systems:

Technical Analysis is based on a study of historical price movements and past trend patterns. There is no assurance that these market changes or trends can or will be duplicated shortly. It logically follows that historical precedent does not guarantee future results. Conclusions expressed in the Technical Analysis section are personal opinions: and may not be construed as recommendations to buy or sell anything.

Disclaimer: The views expressed are not necessarily the view of Sage Point Financial, Inc. and should not be interpreted directly or indirectly as an offer to buy or sell any securities mentioned herein. Securities and Advisory services offered through Sage Point Financial Inc., Member FINRA/SIPC, and an SEC-registered investment advisor.

Past performance cannot guarantee future results. Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Please note that individual situations can vary. Therefore, the information presented in this letter should only be relied upon when coordinated with individual professional advice. *There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment. No investment strategy, such as asset allocation, can guarantee a profit or protect against loss in periods of declining values. It is our goal to help investors by identifying changing market conditions. However, investors should be aware that no investment advisor can accurately predict all of the changes that may occur in the market. The price of commodities is subject to substantial price fluctuations of short periods and may be affected by unpredictable international monetary and political policies. The market for commodities is widely unregulated, and concentrated investing may lead to Sector investing may involve a greater degree of risk than investments with broader diversification. Indexes cannot be invested indirectly, are unmanaged, and do not incur management fees, costs, and expenses.

Dow Jones Industrial Average: A weighted price average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ. S&P 500: The S&P 500 is an unmanaged indexed comprised of 500 widely held securities considered to be representative of the stock market in general.

NASDAQ: the NASDAQ Composite Index is an unmanaged, market-weighted index of all over the counter common stocks traded on the National Association of Securities Dealers Automated Quotation System (IWM) I Shares Russell 2000 ETF: Which tracks the Russell 2000 index: which measures the performance of the small capitalization sector of the U.S. equity market.

A Moderate Mutual Fund risk mutual has approximately 50-70% of its portfolio in different equities, from growth, income stocks, international and emerging markets stocks to 30-50% of its portfolio in different categories of bonds and cash. It seeks capital appreciation with a low to moderate level of current income.

The Merrill Lynch High Yield Master Index: A broad-based measure of the performance of non-investment grade US Bonds

MSCI EAFE: the MSCI EAFE Index (Morgan Stanley Capital International Europe, Australia, and Far East Index) is a widely recognized benchmark of non-US markets. It is an unmanaged index composed of a sample of companies’ representative of the market structure of 20 European and Pacific Basin countries and includes reinvestment of all dividends. Investment grade bond index: The S&P 500 Investment-grade corporate bond index, a sub-index of the S&P 500 Bond Index, seeks to measure the performance of the US corporate debt issued by constituents in the S&P 500 with an investment-grade rating. The S&P 500 Bond index is designed to be a corporate-bond counterpart to the S&P 500, which is widely regarded as the best single gauge of large-cap US equities.

Floating Rate Bond Index is a rule-based, market-value weighted index engineered to measure the performance and characteristics of floating-rate coupon U.S. Treasuries, which have a maturity greater than 12 months.

Money Flow; The Money Flow Index (MFI) is a momentum indicator that measures the flow of money into and out of a security over a specified period. It is related to the Relative Strength Index (RSI) but incorporates volume, whereas the RSI only considers SK-SD Stochastics. When an oversold stochastic moves up through its MA, a buy signal is produced. Furthermore, Lane recommends that the stochastic line be smoothed twice with three-period simple moving averages: SK is the three-period simple moving average of K, and SD is the three-period simple moving average of SK

Rising Wedge; A rising wedge is a technical indicator, suggesting a reversal pattern frequently seen in bear markets. This pattern shows up in charts when the price moves upward with pivot highs and lows converging toward a single point known as the apex

The 2020 COVID-19 Virus has adversely affected the entire world, and this will go down as one of the most volatile years in the stock and bond market in generations and even more volatile than the 2008 Bear Market.

CURRENT MARKET CONDITIONS:

This reason is that the declines came over eight days and not like the 2007-2009 decline which took a year and one half. The great recession of 2008 was a humanmade financial problem and this is a virus where very few are working. In the Recession of 2008, people were at least going to work and going out and spending money to support the economy. Now we are all destined to stay in the house unless we have an essential business. But the U.S. Government is doing everything it can to give grants and forgivable loans so that the economy doesn’t totally crash. That is better than in 2008. It is still serial to be confined to your house or go for a walk.

When we get our statement of our investments from our 401(k) s or from these accounts, you will see pretty large drops in values in the investment account and you will wonder if this is all worth it to stay in it or are we all destined just to make 1-3% in a savings account or a 3% fixed annuity with me. Right now getting 3% with no fees looks pretty good.

If you believe that good stocks and funds from successful growing businesses do well over the long term and this sell-off in the markets are BUYING opportunities over the next few months you may want to dollar cost average into the markets. If you believe that this COVID-19 virus will soon be over within months and that 1 to 3 years from now the markets will be higher than they are now is it worth holding on OR Buying more when markets are lower? The question is if you are buying or investing for the next 1-20 years. Do you like suitable stock and bond investments that are cheap now or more expensive? If your answer is yes, than you may want to average into the markets over the next few months as it is down during this pandemic.

MARKET RECAP:

On my last 3 Bartometers I was getting and got Very Cautious about the stock and bond markets, but did I expect this? Not really. I said if the NASDAQ broke 9200, I will get very Cautious but a 25 to 35% decline I did not expect. The markets had rallied 20%+ from the low hit a couple of weeks ago but still, the markets are down 17-20% into 2020. Are we in a recession now? I’d say yes, but it is forced because of COVID-19, but it will be one just because of the number of people laid off.

In the following pages are discussions of the long term of the markets, what do in a Bear market and my technicals of the markets going forward. But above I would like to say that even though American Capitalism is under fire, and also though the market got hurt as well as our portfolios, we will rise to the COVID-19 challenge like any other war or attack on the United States of America going back to the Revolutionary War to WW1, WW2, and all the other wars we had in our history. This country and its citizens will find a vaccine to this virus and I believe in my heart that 1 to 2 years from now this market should be nicely higher. Dollar-cost averaging currently buying a lower priced shares of good companies should, with no guarantees expressed or implied, be a good deal higher over the next few years. What do you think? Have we gone down this much over the last 50 years? Yes, many times. Has it recovered each time? Yes. Because capitalism works and good companies over the long term make money.

Some of the INDEXES of the markets both equities and interest rates are below. The source is Morningstar.com up until April 7, 2020. These are passive indexes. *Dow Jones -20% S&P 500 -17% NASDAQ Aggressive growth -9% I Shares Russell 2000 ETF (IWM) Small cap -31% Midcap stock funds -29% International Index (MSCI – EAFE ex USA -22% Investment Grade Bond -4% High Yield Bond -13% Government bond +4% The average Moderate Fund is down -16% this year fully invested as a 65% in stocks and 35% in bonds and nothing in the money market.

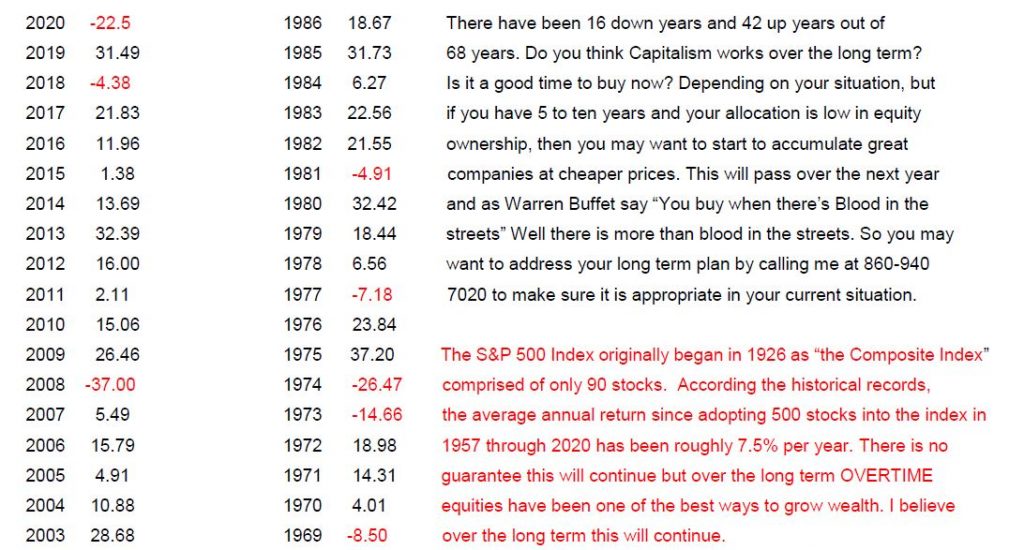

WANT TO SHOW YOU THE YEAR BY YEAR RETURNS OF THE S&P 500 TOTAL RETURNS BY YEAR

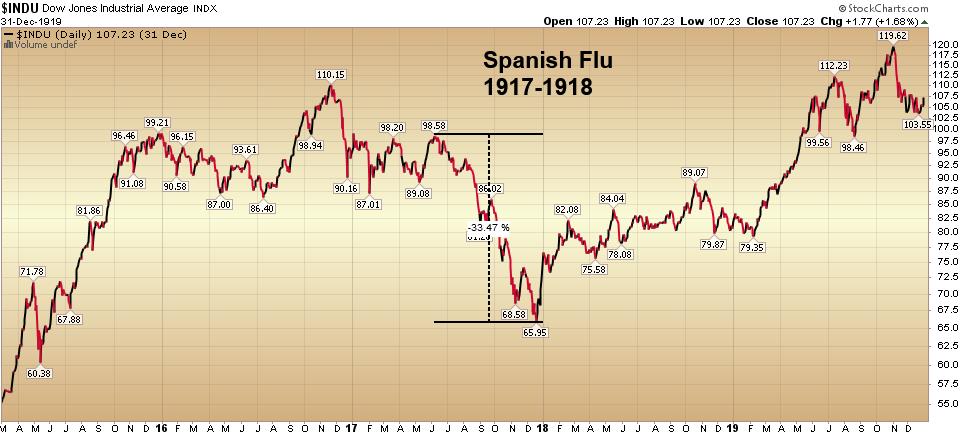

WHAT HAPPENED TO THE MARKETS DURING THE PANDEMIC AND SPANISH FLU IN 1917-1918:

The stock market today is looking a lot like it did a century ago, and if Great Hill Capital’s Thomas Hayes’s interpretation of the trendlines is on point, the bottom could be approaching.

“Just as the market started discounting the worst-case scenario in 1917,” he wrote, “it was already discounting a recovery months before the worst-case scenario occurred in 1918.”

What was going on in 1917? The Spanish Flu was just starting to bubble up, with the deadliest month of the whole pandemic not hitting until October 1918 — by then, as you can see from this chart, the Dow Jones Industrial Average DJIA, -1.68% had already begun to heal.

Hayes then posted this chart of the modern-day market plunge, noting that the nasty drawdowns amid the early stages of both pandemics were virtually the same.

More than 51 million people died globally in the Spanish Flu Pandemic, and the market rebounded more than 80% in the following two years from its bottom to top. This is no guarantee the market will rally that much or at all, but the USA is now better equipped to handle a massive Pandemic then in 1918 to 1919. Also, many companies are internet companies that could do well as people shop and do business over the internet; in addition, it is much more diversified and global than it was in 1918. For these reasons and more, I believe that the long term is more promising now for a recovery over the next 1 to 2 years.

There is one caveat; the Commodity index is right near its low of 2009, where it found it at a 29-year support level. If that breaks through that level, then we can go into a deeper recession for a more extended period. The market rebound depends on how quickly the government fixes this problem and people go back to work. I am optimistic over the next two years; but understand a recession should happen at least for a few quarters. I think the Recession should be relatively short term.

Since this graph was made a week ago, look at the next page and it is up to date. COMPARE the next graph to the Pandemic of 1918 and it is starting to look more like it. There is no guarantee expressed or implied, but look at the Pandemic and then the updated Dow on the next page.

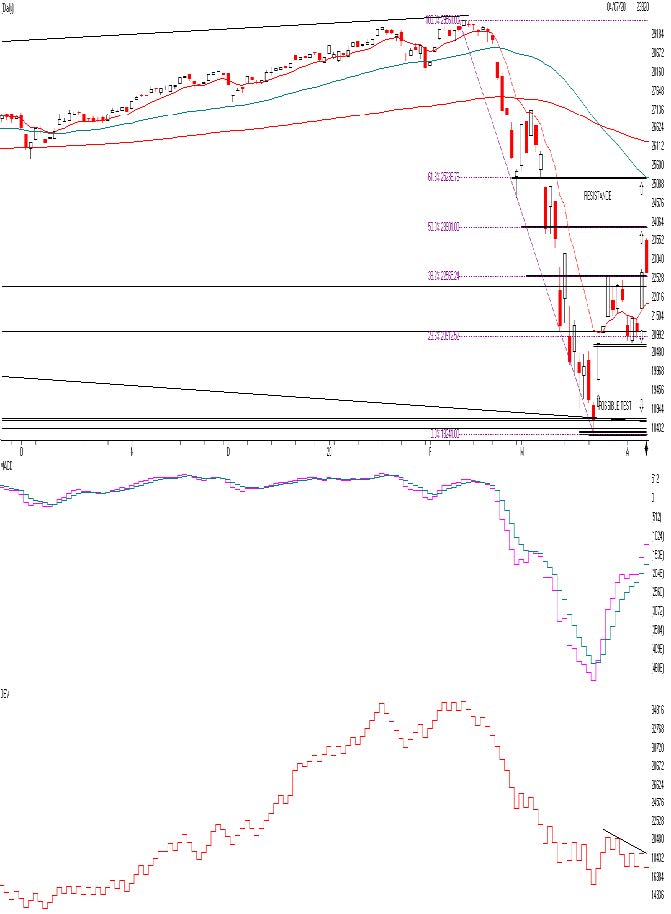

The Dow Jones is above. This is the Daily Chart. As you can see, the decline of the Dow Jones Average was relatively very quick. Current is sitting at 22653 right BELOW THE 50% Fibonacci retracement level. A normal BEAR market usually tops on a countertrend rally right at a 50% or 61.8% Fibonacci level and declines or puts in a short top. So if this is true in this case there could be resistance at 23,901 or 25,236 area. There is also some resistance at the 200 day moving average at 26,660 and sloping downward. My AIQ models gave a BUY on 3/24/2020, but only a short term Buy not a longer term Weekly Buy. So even though the market is somewhat short term Bullish, there could be a short term top at 23,901, 25,236 or the 26,660 areas.

Momentum is good but can change quickly on the downside after earnings come out that will be bad. A buy signal is giving when the lavender line crosses blue line and Sell signal when it does it on the downside

One thing I don’t like is the On Balance Volume Line. Notice as the market is going up it is going up on low relative volume. This is somewhat negative. Over all I think the market should be higher when this is all done and when there is a vaccine and people go on living their normal lives it should be better. This market will be volatile. The market may continue on the upside but over the short term I think the rally is limited to the levels I said above on the Fibonacci levels and the 200 day moving average. In addition, the market may not like the earnings numbers over the next couple of weeks and the market could drop again towards 20000 or below again.

Key investor Points to remember in a Bear Market:

Stay calm and keep a long-term perspective.

Maintain a balanced and broadly diversified portfolio.

Balance equity portfolios with a mix of dividend-paying companies and growth stocks.

Choose funds with a strong history of weathering market declines.

Use high-quality bonds to help offset equity volatility.

Advisors can help investors navigate periods of market volatility

THE BOTTOM LINE:

The market has had its worst decline in 10 years. It has recovered about 35% of the loss over the last week. It is not a time to sell during this decline in my opinion but for some of you it would a great time to start to nibble in your mutual funds on setbacks because the COV19 virus should be controlled over the next year and if you look at all of the virus pandemics we have had, it has been a good time to Buy if your goals are longer term. It is not a time to throw caution to the wind but call me to make selective dollar-cost average buys. In addition, when EARNINGS come out in the next 2 weeks the stock market could go back down again. Remember you buy when there is blood in the streets. Bonds should be more in the investment-grade or short- term investment grade side. If you are a long-term investor and have 20 years+ towards retirement use sell-offs to add through dollar-cost averaging. Diversification is essential but portfolios should be somewhat safer.

Best to all of you,

Joe Bartosiewicz, CFP® Investment Advisor Representative 5 Colby Way Avon, CT 06001 860-940-7020 or 860-404-0408

SECURITIES AND ADVISORY SERVICES OFFERED THROUGH SAGE POINT FINANCIAL INC., MEMBER FINRA/SIPC, AND SEC-REGISTERED INVESTMENT ADVISOR.

Charts provided by AIQ Systems:

Technical Analysis is based on a study of historical price movements and past trend patterns. There is no assurance that these market changes or trends can or will be duplicated shortly. It logically follows that historical precedent does not guarantee future results. Conclusions expressed in the Technical Analysis section are personal opinions: and may not be construed as recommendations to buy or sell anything.

Disclaimer: The views expressed are not necessarily the view of Sage Point Financial, Inc. and should not be interpreted directly or indirectly as an offer to buy or sell any securities mentioned herein. Securities and Advisory services offered through Sage Point Financial Inc., Member FINRA/SIPC, and an SEC-registered investment advisor.

Past performance cannot guarantee future results. Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Please note that individual situations can vary. Therefore, the information presented in this letter should only be relied upon when coordinated with individual professional advice. *There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment. No investment strategy, such as asset allocation, can guarantee a profit or protect against loss in periods of declining values. It is our goal to help investors by identifying changing market conditions. However, investors should be aware that no investment advisor can accurately predict all of the changes that may occur in the market. The price of commodities is subject to substantial price fluctuations of short periods and may be affected by unpredictable international monetary and political policies. The market for commodities is widely unregulated, and concentrated investing may lead to Sector investing may involve a greater degree of risk than investments with broader diversification. Indexes cannot be invested indirectly, are unmanaged, and do not incur management fees, costs, and expenses.

Dow Jones Industrial Average: A weighted price average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ. S&P 500: The S&P 500 is an unmanaged indexed comprised of 500 widely held securities considered to be representative of the stock market in general.

NASDAQ: the NASDAQ Composite Index is an unmanaged, market-weighted index of all over the counter common stocks traded on the National Association of Securities Dealers Automated Quotation System (IWM) I Shares Russell 2000 ETF: Which tracks the Russell 2000 index: which measures the performance of the small capitalization sector of the U.S. equity market.

A Moderate Mutual Fund risk mutual has approximately 50-70% of its portfolio in different equities, from growth, income stocks, international and emerging markets stocks to 30-50% of its portfolio in different categories of bonds and cash. It seeks capital appreciation with a low to moderate level of current income.

The Merrill Lynch High Yield Master Index: A broad-based measure of the performance of non-investment grade US Bonds

MSCI EAFE: the MSCI EAFE Index (Morgan Stanley Capital International Europe, Australia, and Far East Index) is a widely recognized benchmark of non-US markets. It is an unmanaged index composed of a sample of companies’ representative of the market structure of 20 European and Pacific Basin countries and includes reinvestment of all dividends. Investment grade bond index: The S&P 500 Investment-grade corporate bond index, a sub-index of the S&P 500 Bond Index, seeks to measure the performance of the US corporate debt issued by constituents in the S&P 500 with an investment-grade rating. The S&P 500 Bond index is designed to be a corporate-bond counterpart to the S&P 500, which is widely regarded as the best single gauge of large-cap US equities.

Floating Rate Bond Index is a rule-based, market-value weighted index engineered to measure the performance and characteristics of floating-rate coupon U.S. Treasuries, which have a maturity greater than 12 months.

Money Flow; The Money Flow Index (MFI) is a momentum indicator that measures the flow of money into and out of a security over a specified period. It is related to the Relative Strength Index (RSI) but incorporates volume, whereas the RSI only considers SK-SD Stochastics. When an oversold stochastic moves up through its MA, a buy signal is produced. Furthermore, Lane recommends that the stochastic line be smoothed twice with three-period simple moving averages: SK is the three-period simple moving average of K, and SD is the three-period simple moving average of SK

Rising Wedge; A rising wedge is a technical indicator, suggesting a reversal pattern frequently seen in bear markets. This pattern shows up in charts when the price moves upward with pivot highs and lows converging toward a single point known as the apex

Over the last month the stock market has had one of its worst declines over the shortest periods of time in history. Not even did the 2008 declines beat the velocity of the declines we saw over the last month. In 2 days the NASDAQ fell over almost 11% because of the rightfully so, Corona Virus and its potential to not only kill people but mainly do disrupt the business process of selling and the supply lines to get product. Two things I do want to say is

1. You don’t base your long term financial goals based on a short term flu. 5 years from now this will be just another flu we had. People will have forgotten about it.

2. Over the last two months I have be saying to take profits as we were overvalued, I was getting Cautious with the Rising Wedge pattern and thought the S&P 500 would go to the 3280-3380 and top out. The S&P 500 topped at 3386 and fell through the trend lines to the 2900 area, down 13% from the 3380 level. As of this point I am still very Cautious, but looking for a bottom soon over the next 2 months.

This is why I do technical analysis. People can say that the Corona Virus did it, and it did contribute, but the market was positioning itself for a fall. I think the market will continue to be volatile and potentially fall more. With the outbreak just beginning the USA, the S&P should test the 2855 level it hit a week ago and either bounce from there but I feel it will probably break down below that and hit the 2600 to the 2750 level. There have only been less than 500 people who have gotten the tests. Once the US government opens the tests up to many more people there should be many many more people who have the virus. This will scare people to stop going out at restaurants, coffee shops, theatres, cruise ships, travel and more. It will take out a percentage out of the Gross Domestic Product, (GDP). It will probably cause the markets to fall another 5 to 10%+, but it will not kill Capitalism. It should only be a short term. Remember, if this is a flu where less than 1% of the people who contract it dies, then who are dying? The elderly and the sick who have immune problems. So protect yourself. Get the N95 masks on Amazon, get myricetin as a supplement people are recommending to build up your immune system. Talk to your doctor first. Call me to rearrange your portfolios with me and your 401(k). Remember too, this will pass, but I think we have more on the downside.

This is what’s happened over the last 20 years:

2000 Y2k is going to kill us all.

2001 Anthrax is going to kill us all.

2002 West Nile Virus is going to kill us all.

2003 SARS is going to kill us all.

2005 The Bird Flu is going to kill us all. 2008 The Great Recession is going to kill us all.

2010 BP Oil is going to kill us all.

2012 The Mayan Calendar is going to kill us all.

2013 North Korea is going to kill us all.

2014 Ebola is going to kill us all.

2015 Disney Measles and ISIS is going to kill us all.

2016 Zika virus is going to kill us all.

2020 Corona Virus is going to kill us all.

Now granted this is worse because it is a pandemic and it is worse than most of the others, not in life as we lose 30-60 thousand every year to the regular flu, but there is no vaccine yet, and it is creating FEAR. But mostly the FEAR is stopping people from spending money, this will cause the markets to fall. So FEAR is killing you. Protect yourself. Be smart. Use FEAR in the markets as an advantage. Over the last few months, go to the old Bartometers, I have been saying to take profits, the markets are too overbought, that we had a Rising Wedge formation that is a reversal pattern and I thought we could go down. Well now that that has happened, is the market a BUY yet? No, because I feel it will go down more, but it may bottom over the next month or two.

There may be buying opportunities that only come once every 10 years or so. With no guarantees, if the market goes below the 2855 level down to the 2600 level to the 2750 level you may want to call me for potential buying opportunities. Remember what Warren Buffet says, “ Buy when there is BLOOD in the STREETS” That’s when most make money over the long term, When Florida houses were plummeting in the 2008 recession, were there great BUYS? In the great recession, did stocks go so low that if you bought in early 2009 did you get unbelievable deals on stocks and funds? Yes… You make money in the bull markets by buying in the BEAR MARKETS. I am not saying to buy now but get your GREED hats on. You all need to contact me to discuss strategy now. Remember, can we go down more? YES and probably will. Can we go into a Recession because of this situation? Maybe and most likely, economists are giving it a 50-50% chance. Should you reduce equities more, possibly depending on your situation and how close you are to retirement? Last month I said to take money off the table because the markets were too high. Now it’s more of a shift between funds and change some of the bonds as if Oil keeps falling, you don’t want to have much in the High Yield Bond sector or Floating rate bond area. I am concerned, however, about the corporations continue to buy back their own shares while they are issuing debt to do it. This buying back of stock is building the asset bubble. This is one concern I have in addition Corona Virus.

An excerpt from Fundamental Economist Dr. Robert Genetski: from Classical Principles.com: Stock Market Volatile as the Virus Gains

Investors switched from euphoria to fear and back several times this past week. When the dust settled, the Nasdaq, Nasdaq 100 and S&P 500 rose 1%-3% while small cap stocks fell 1%-2%.

The reason I recommend caution is related to the expectation of a sharp increase in the virus in the US. The US conducted only 473 tests through March 1. The number of tests will increase dramatically in the period ahead. More testing means more confirmed cases. The latest figures for the US show 226 cases.

Outside the US infections are growing at a rate of 20% a day. The rate of increase has slowed in Korea, but has increased dramatically in Italy and throughout Europe.

There is some good news. The daily rate of increase in China has slowed to less than 0.2% for the four days ending March 5th. Flexport, a global freight logistics company, reports that 60% of China’s manufacturing capacity is now back on line. Since US companies depend on China for critical supplies and medicines, the threat of shortages should soon be less pressing. There was more good news this past week as surveys of business activity show the US economy remained remarkably strong in February. While various international companies are suffering greatly, recent indications show the US is weathering the storm well, at least through February. Amid the uncertainty over the spread of the virus in the US, it continues to make sense to be cautious about owning stocks.

Returns in 2020 Some of the INDEXES of the markets both equities and interest rates are below. The source is Morningstar.com up until March 7, 2020. These are passive indexes.

*Dow Jones -8.9% S&P 500 -8.2% NASDAQ Aggressive growth -4.4% I Shares Russell 2000 ETF (IWM) Small cap -12.84% Midcap stock funds -12.54% International Index (MSCI – EAFE ex USA -10.4% Moderate Mutual Fund Investment Grade Bonds (AAA) Long duration -4.70% High Yield Merrill Lynch High Yield Index -3.7%

Floating Rate Bond Funds -2.4% Short Term Bond +1.3% Fixed Bond Yields (10 year) .76% Yield

The average Moderate Fund is down -4.70% this year fully invested as a 65% in stocks and 35% in bonds and nothing in the money market.

Interest rates look stable going forward over the next 6 months

The S&P 500 is above. I used a weekly chart as I think the S&P will fall below 2855 and possibly hit the following support levels for support. 2822, 2721-2747, 2600-2630, and 2340.

These are points that investors are looking at as a support levels. I think we have more to go on the downside. The Blue arrows are areas that listed to the left I think the S&P can go too.

The middle graph is the SK-SD stochastics. This shows a breakdown, Last month I said anything over the 88 level is overbought. It’s 21 to 48 on the Daily, now it’s getting OVERSOLD but can go down more.

The third graph is the Stochastics chart. Anything below 20 is showing the market is very oversold. But can still trend lower.

The Dow Jones is above. I drew the last three years and notice the that the 23576 is support right at the red line , but I believe the low will breakdown as it could test and breakdown and test its 200 week moving average at 23,587. If that doesn’t hold then the old lows of 21,734 are next.

This could be the capitulation investors are looking at to starting getting back into the markets. If this happens then there is a much greater chance that a Recession will occur. Please call me to Strategize your portfolio at 860-940-7020.

Support levels on the S&P 500 area are 2822, 2721-2747, 2600-2630 and 2340. These might be accumulation areas if you are a Long term investor. Support levels on the NASDAQ are 7658 to 7715, 7303, and 6861. On the Dow Jones support is at 23,587 (200 week moving average), 21,734, 19,794 and 17,863 These may be safer areas to get into the equity markets on support levels slowly.

THE BOTTOM LINE: Now that the markets have broken down the trend line I explained last month. I am more Cautious on the markets. The Corona Flu will scare people and they will pull in their horns towards traveling, going out and this act alone can cause a Recession. The market is starting to become somewhat oversold but I still would no Buy here, but wait until the Corona Virus Fear is nearing the worst it could get. That could be over the next 2 months or so. I think the S&P 500 and the markets could continue to fall as energy is also going down.

Best to all of you,

Joe Bartosiewicz, CFP® Investment Advisor Representative Contact information:

5 Colby Way Avon, CT 06001 860-940-7020 or 860-404-0408

SECURITIES AND ADVISORY SERVICES OFFERED THROUGH SAGE POINT FINANCIAL INC., MEMBER FINRA/SIPC, AND SEC-REGISTERED INVESTMENT ADVISOR.

Charts provided by AIQ Systems: Technical Analysis is based on a study of historical price movements and past trend patterns. There is no assurance that these market changes or trends can or will be duplicated shortly. It logically follows that historical precedent does not guarantee future results. Conclusions expressed in the Technical Analysis section are personal opinions: and may not be construed as recommendations to buy or sell anything.

Disclaimer: The views expressed are not necessarily the view of Sage Point Financial, Inc. and should not be interpreted directly or indirectly as an offer to buy or sell any securities mentioned herein. Securities and Advisory services offered through Sage Point Financial Inc., Member FINRA/SIPC, an SEC-registered investment advisor.

Past performance cannot guarantee future results. Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Please note that individual situations can vary. Therefore, the information presented in this letter should only be relied upon when coordinated with individual professional advice. *There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment. No investment strategy, such as asset allocation, can guarantee a profit or protect against loss in periods of declining values.

It is our goal to help investors by identifying changing market conditions. However, investors should be aware that no investment advisor can accurately predict all of the changes that may occur in the market.

The price of commodities is subject to substantial price fluctuations of short periods and may be affected by unpredictable international monetary and political policies. The market for commodities is widely unregulated, and concentrated investing may lead to Sector investing may involve a greater degree of risk than investments with broader diversification.

Indexes cannot be invested indirectly, are unmanaged, and do not incur management fees, costs, and expenses.

Dow Jones Industrial Average: A weighted price average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ.

S&P 500: The S&P 500 is an unmanaged indexed comprised of 500 widely held securities considered to be representative of the stock market in general.

NASDAQ: the NASDAQ Composite Index is an unmanaged, market-weighted index of all over the counter common stocks traded on the National Association of Securities Dealers Automated Quotation System

(IWM) I Shares Russell 2000 ETF: Which tracks the Russell 2000 index: which measures the performance of the small capitalization sector of the U.S. equity market.

A Moderate Mutual Fund risk mutual has approximately 50-70% of its portfolio in different equities, from growth, income stocks, international and emerging markets stocks to 30-50% of its portfolio in different categories of bonds and cash. It seeks capital appreciation with a low to moderate level of current income.

The Merrill Lynch High Yield Master Index: A broad-based measure of the performance of non-investment grade US Bonds

MSCI EAFE: the MSCI EAFE Index (Morgan Stanley Capital International Europe, Australia, and Far East Index) is a widely recognized benchmark of non-US markets. It is an unmanaged index composed of a sample of companies’ representative of the market structure of 20 European and Pacific Basin countries and includes reinvestment of all dividends.

Investment grade bond index: The S&P 500 Investment-grade corporate bond index, a sub-index of the S&P 500 Bond Index, seeks to measure the performance of the US corporate debt issued by constituents in the S&P 500 with an investment-grade rating. The S&P 500 Bond index is designed to be a corporate-bond counterpart to the S&P 500, which is widely regarded as the best single gauge of large-cap US equities.

Floating Rate Bond Index is a rule-based, market-value weighted index engineered to measure the performance and characteristics of floating-rate coupon U.S. Treasuries, which have a maturity greater than 12 months.

Money Flow; The Money Flow Index (MFI) is a momentum indicator that measures the flow of money into and out of a security over a specified period. It is related to the Relative Strength Index (RSI) but incorporates volume, whereas the RSI only considers

SK-SD Stochastics. When an oversold stochastic moves up through its MA, a buy signal is produced. Furthermore, Lane recommends that the stochastic line be smoothed twice with three-period simple moving averages: SK is the three-period simple moving average of K, and SD is the three-period simple moving average of SK

Rising Wedge; A rising wedge is a technical indicator, suggesting a reversal pattern frequently seen in bear markets. This pattern shows up in charts when the price moves upward with pivot highs and lows converging toward a single point known as the apex

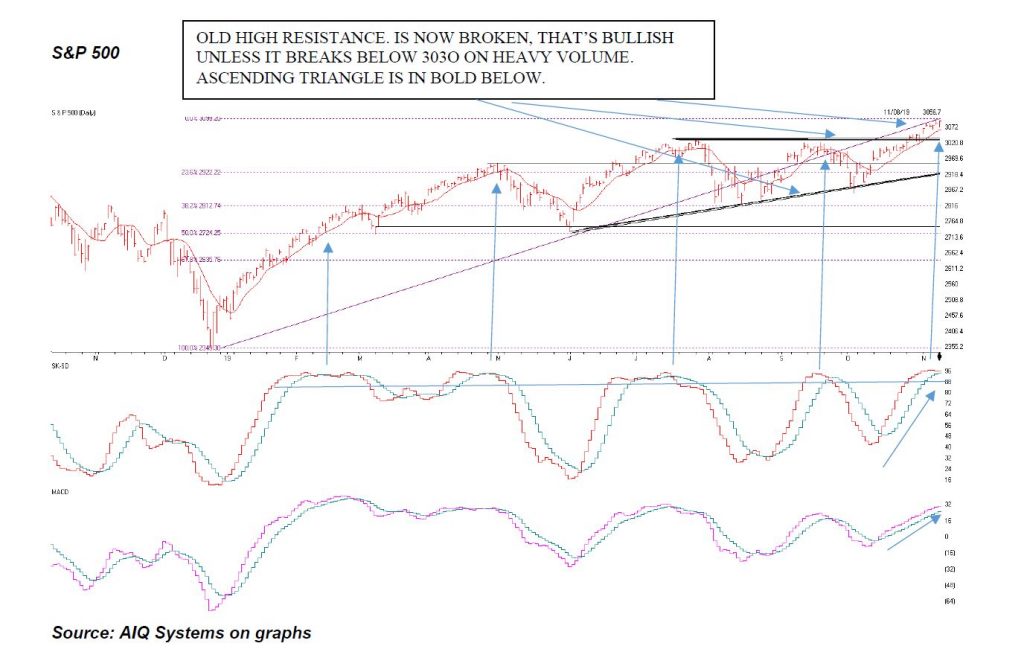

On my last Bartometer I stated that we were #1 On Buy signal, #2 the Dow Jones and the stock market had Bullish Ascending triangles patterns, #3. Money flow and On Balance Volume were breaking out to NEW HIGHS when the stock market wasn’t. This shows demand for stocks over and above the price. These 3 indicators were telling me and I was telling you that I thought the market would breakout to new highs, AND IT DID. The stock market broke out of the bullish ascending triangle, (see index on the next page about ascending triangles)*. On the S&P I said that it had to breakout of 3030 and it did. It is now 3093. I said the Dow Jones had to breakout of the 27400, and it did. It is now 27681.

Where does is go from here and could we get a little pull back?

See chart below for an explanation.

An excerpt from Fundamental Economist Dr. Robert Genetski: from Classical Principles.com:

Stocks benefited from encouraging news of a potential trade agreement between the US and China as well as some good news on the economy. Markets seldom move in only one direction. The S&P500 is now within 3% of its fundamental value. A pause or even a slight correction is overdue, particularly if there is any negative news. Even so, with stronger fundamentals and the Fed purchasing securities, any correction should be fairly mild. Stay bullish on stocks.

Adding to Bob’s his Comment:

Signs of strength in the economy combined with gains in stock prices led to a sharp jump in intermediate and longer-term interest rates. This week the interest rate on 10-year T-Notes moved 25 basis points higher. The latest moves turned the yield curve to a more normal shape. As with stocks, interest rates have spiked higher and are overdue for some correction. However, after more than a decade of interest rates declining and being well below their fundamental levels, rates remain 200 basis points below fundamental levels. While the Fed’s low target places a limit on how high interest rates will go, there is still a lot of upward potential for longer-term rates. Fixed-income portfolios should remain defensive.

On the Technical Side:

Over the last almost 22 months, the Dow Jones FINALLY broke out to new highs from the old highs set on Jan 31, 2018 at 26,714. That is a POSITIVE. Money Flow and On Balance Volume are still at a new high, but the markets are again becoming overbought. So, could the market comes down a little now? YES, the markets are now overbought and there could easily be a slight decline to 27191 to 27298, a decline of around 2%, and the S&P to decline to 3029 area, a decline of 2% or so, BUT no more than that, because if the markets GO BACK BELOW THE BREAKOUT it can cause traders to start selling in mass. So look for a possible test of the breakout, but IF the markets close below the breakout of 27300 to 27384 on the Dow Jones or 3030 on the S&P convincingly, then I will be getting Very Cautious. If that doesn’t happen then I am still moderately bullish. But I realize the market are now OVERBOUGHT and in my opinion, it is not a time to go out and invest a lot of money in the markets. Dollar cost averaging is fine. I stated in my January Bartometer that I thought the S&P could reach 3130 to 3180+ this year. At 3093 currently, that is about 1-3% from here.

Some of the INDEXES of the markets both equities and interest rates are below. The source is Morningstar.com up until November 9th, 2019. These are passive indexes. *Dow Jones +20% S&P 500 +24% NASDAQ Aggressive growth +31% I Shares Russell 2000 ETF (IWM) Small cap +19% International Index (MSCI – EAFE ex USA) +16% Moderate Mutual Fund +14% Investment Grade Bonds (AAA) +13% High Yield Merrill Lynch High Yield Index +11% Floating Rate Bond Index +4.0% Short Term Bond +4.0% Fixed Bond Yields (10 year) +1.75.% Yield

The average Moderate Fund is up 14% this year fully invested as a 60% in stocks and 40% in bonds and nothing in the money market.

S&P 500

Ascending Triangle is above, and is Bullish as long as it stays above the breakout of 3027-3030

The S&P 500 is above. The S&P 500 contains 500 of the largest companies in the US. The 2 top companies by market value are Microsoft and Apple. But there are 498 other stocks in it. If you can see above the ASCENDING TRIANGLE that is BOLDED. Notice the clear breakout to new highs. This is clearly BULLISH like I thought would happen last month. And it did. Now that it has risen 2% ABOVE the breakout, a BREAKDOWN below the 3030 convincingly would get me VERY Cautious. It is normal to come back down to test the breakout, but not to break down below it. So if you see the S&P close below 3030 convincingly on heavy volume, I will be getting Cautious to Very Cautious depending on the reason. But the market is now at fair value to me and there may be another 1-4% more for the year in my opinion, but not much more unless there is incredible news from the Political or Tariff front. It is not a great time to go out and buy a lot in the stock market in my opinion as well.

The Middle graph is called the SK-SD Stochastics model. It shows the markets as being overbought when the indicator is above 88 where it is above the 88 horizontal line. Notice every time the indicator was above 88 it seemed to peak out and sell off. This is not guaranteed but it is good indicator.

The 3rd indicator is MACD or Momentum this indicator is still bullish until the pink line breaks down below the blue line. As of right now, momentum is still higher, but the markets are over bought, so be careful.

An ascending triangle is a chart pattern used in technical analysis. It is created by price moves that allow for a horizontal line to be drawn along the swing highs, and a rising trend line to be drawn along the swing lows. The two lines form a triangle. Traders often watch for breakouts from triangle patterns.

See the pattern above? It’s an Ascending triangle. Ascending triangles are BULLISH as long as they don’t go back below the breakout. If this is a successful Ascending triangle the S&P can rise to 3130-3180 first and possibly higher IF the breakout isn’t broken convincingly on the downside or breaking and closing below 3030.

On-balance volume (OBV) is a technical analysis indicator intended to relate price and volume in the stock market. OBV is based on a cumulative total volume.

Money flow is calculated by averaging the high, low and closing prices, and multiplying by the daily volume. Comparing that result with the number for the previous day tells traders whether money flow was positive or negative for the current day. Positive money flow indicates that prices are likely to move higher, while negative money flow suggests prices are about to fall.

A Support or support level is the level at which buyers tend to purchase or into a stock or index. It refers to the stock share price that a company or index should hold and start to rise. When the price of the stock falls towards its support level, the support level holds and is confirmed, or the stock continues to decline, and the support level must change.

Support levels on the S&P 500 area are 3027-3030, 3017, 2952, 2922, and 2812. These might be BUY areas.

Support levels on the NASDAQ are 8251, 8144, 8080 and 7771.

On the Dow Jones support is at 26,285, 25,763, and 25,458

These may be safer areas to get into the equity markets on support levels slowly.

RESISTANCE LEVEL ON THE S&P 500 IS 3130 and the Dow Jones breakout is 27,400. If there is a favorable tariff settlement, the market should rise short term.

THE BOTTOM LINE:

The Dow, the S&P 500 and the NASDAQ are at new highs after rallying over the last 3 weeks. Normally the markets after reaching new highs become overbought and may come back down towards the breakout areas to see if the breakouts area holds. lf breakout of 3030 are holds then the markets tend to drift back towards the old high to see if it can break out again. If it does then 3130 to 3180 could be the next target. If 3030 doesn’t hold on the S&P and starts to break down below 3030 then I will be getting cautious or very cautious.. I WILL CONTINUE TO ANALYZE THE TECHNICALS OF THE MARKET. The seasonal patterns of the markets are bullish towards the end of the year. Last year the markets fell in December. It looks like the market still wants to go up, but with tweets coming out hourly, market timing will be more difficult.

Best to all of you,

Joe Bartosiewicz, CFP®

Investment Advisor Representative 5 Colby Way Avon, CT 06001 860-940-7020 or 860-404-0408

SECURITIES AND ADVISORY SERVICES OFFERED THROUGH SAGE POINT FINANCIAL INC., MEMBER FINRA/SIPC, AND SEC-REGISTERED INVESTMENT ADVISOR.

Charts provided by AIQ Systems:

Technical Analysis is based on a study of historical price movements and past trend patterns. There is no assurance that these market changes or trends can or will be duplicated shortly. It logically follows that historical precedent does not guarantee future results. Conclusions expressed in the Technical Analysis section are personal opinions: and may not be construed as recommendations to buy or sell anything.

Disclaimer: The views expressed are not necessarily the view of Sage Point Financial, Inc. and should not be interpreted directly or indirectly as an offer to buy or sell any securities mentioned herein. Securities and Advisory services offered through Sage Point Financial Inc., Member FINRA/SIPC, an SEC-registered investment advisor.

Past performance cannot guarantee future results. Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Please note that individual situations can vary. Therefore, the information presented in this letter should only be relied upon when coordinated with individual professional advice. *There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment. No investment strategy, such as asset allocation, can guarantee a profit or protect against loss in periods of declining values.

It is our goal to help investors by identifying changing market conditions. However, investors should be aware that no investment advisor can accurately predict all of the changes that may occur in the market.

The price of commodities is subject to substantial price fluctuations of short periods and may be affected by unpredictable international monetary and political policies. The market for commodities is widely unregulated, and concentrated investing may lead to Sector investing may involve a greater degree of risk than investments with broader diversification.

Indexes cannot be invested indirectly, are unmanaged, and do not incur management fees, costs, and expenses.

Dow Jones Industrial Average: A weighted price average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ.

S&P 500: The S&P 500 is an unmanaged indexed comprised of 500 widely held securities considered to be representative of the stock market in general.

NASDAQ: the NASDAQ Composite Index is an unmanaged, market-weighted index of all over the counter common stocks traded on the National Association of Securities Dealers Automated Quotation System

(IWM) I Shares Russell 2000 ETF: Which tracks the Russell 2000 index: which measures the performance of the small capitalization sector of the U.S. equity market.

A Moderate Mutual Fund risk mutual has approximately 50-70% of its portfolio in different equities, from growth, income stocks, international and emerging markets stocks to 30-50% of its portfolio in different categories of bonds and cash. It seeks capital appreciation with a low to moderate level of current income.

The Merrill Lynch High Yield Master Index: A broad-based measure of the performance of non-investment grade US Bonds

MSCI EAFE: the MSCI EAFE Index (Morgan Stanley Capital International Europe, Australia, and Far East Index) is a widely recognized benchmark of non-US markets. It is an unmanaged index composed of a sample of companies’ representative of the market structure of 20 European and Pacific Basin countries and includes reinvestment of all dividends.

Investment grade bond index: The S&P 500 Investment-grade corporate bond index, a sub-index of the S&P 500 Bond Index, seeks to measure the performance of the US corporate debt issued by constituents in the S&P 500 with an investment-grade rating. The S&P 500 Bond index is designed to be a corporate-bond counterpart to the S&P 500, which is widely regarded as the best single gauge of large-cap US equities.

Floating Rate Bond Index is a rule-based, market-value weighted index engineered to measure the performance and characteristics of floating-rate coupon U.S. Treasuries, which have a maturity greater than 12 months.